Personal Development, Business, Finance, and Investing for Everyone

An investment in knowledge always pays the best interest.

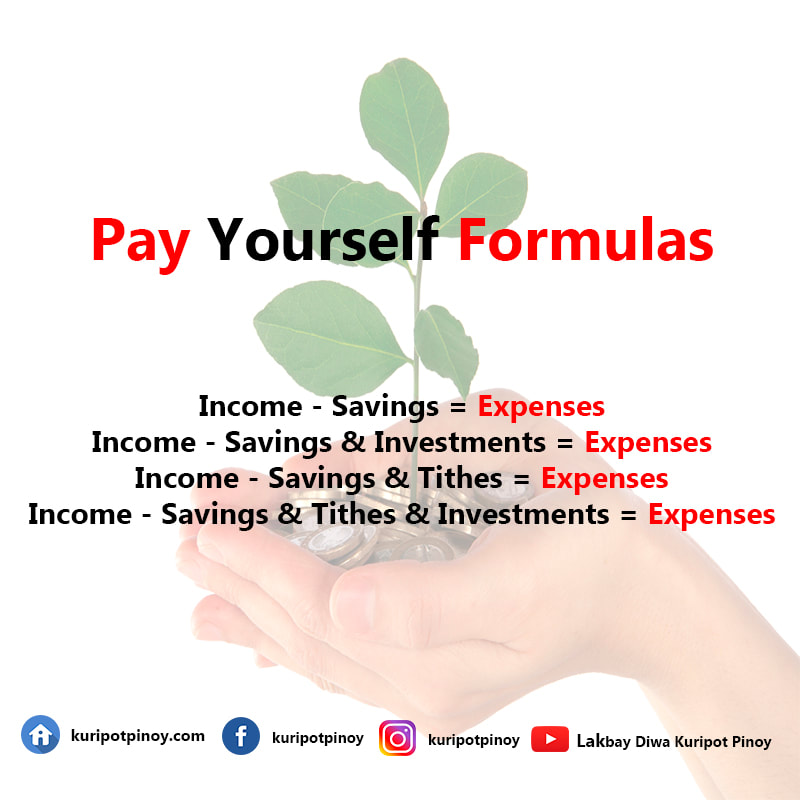

Being in control of your finances is a great stress reliever. All days are not the same. Save for a rainy day. When you don't work, savings will work for you. Every little bit counts, so rather than looking for one big way to save a ton of money, save in lots of small ways and set yourself up for success. As a matter of policy, the BSP (Banko Sentral ng Pilipinas) does not put a ceiling on the amount of fees or charges that banks may collect from their depositors. While banks, as intermediaries of funds between savers and users, play an important role in economic development, they are also business for profit. Thus, banks are given the liberty to impose certain charges. However, these banks have the responsibility to keep their clients aware of relevant bank charges. Disclosure and transparency help clients make informed decision on their banking transactions. How Can I Save On Bank Fees And Charges? Bank Fees, Bank Charges, ATM Transaction Fee, ATM Charges, Interbranch Transaction Fee, Overdraft Charges and Dormancy Fee. How To Save On Bank Fees And Charges Understanding bank fees and charges on deposit are key steps to making the most of your account. If you fail to understand the same, chances are that bank fees and charges are reducing your returns. In order to save on various fees, I suggest that you read the fine prints in the deposit literature and pay closer attention to the following relevant terms and conditions:

Mind The Service Fees Be aware of the different maintenance and transaction fees that banks charge their depositing clients. Some of these fees are service fee for deposits falling below the minimum Average Daily Balance (ADB), dormancy fee, service charge for excess withdrawal, service fee for closing the account within a specified period of time from its opening, ATM transaction fee, overdraft charges, interbranch transaction fee, and others. Awareness of such service fees will help you better manage your deposit account and save on bank fees. Be Watchful Of Your Maintaining Balance Be aware of the required minimum maintaining balance for your account and keep your deposit balance within such maintaining balance. Bank charges/fees for falling below the ADB are computed at the end of each month. In addition, you may also want to take note of the required minimum balance to earn interest, as this may be different from the required minimum maintaining balance. Defend Deposits From Dormancy

Make sure that you update your deposit account regularly. Under BSP regulations, if a savings/current deposit account is left “sleeping” with no transactions (deposits or withdrawals) for a period of two (2) years/one (1) year, it becomes dormant and is subject to dormancy fee. To keep your account active and to avoid this fee, make it a habit to regularly make deposits even in small amounts. However, if this is not possible, it is best to just close the deposit account before the dormancy sets in, no matter how small or big your deposit balance. By this way, you will not to lose your hard-earned money to dormancy fees. Patronize Your Own For free ATM transactions, make sure to use your own bank’s ATMs. You may refer to the bank’s website for a list of its ATM locations. If this is not possible, choose the ATM network with the lowest ATM transaction fee. Bring up to Date Your Checkbook If you maintain a checking account, balance your account as often as you make transactions (e.g. deposit, withdrawals, issuance of checks). It is very important to know how much money you have in your account at all times in order not to “bounce checks”. Typical fees for a check written against insufficient funds range from PhP 1,000.00 to PhP 2,000.00. Think of how much you can possibly save if you make sure that the checks you issued are always funded.

0 Comments

Leave a Reply. |

PLACE YOUR ADS HERE YOUR PAYDAY REMINDER

FEATURED PARTNER

FEATURED PROMOTIONS

FEATURED MENTIONS

PLACE YOUR ADS HERE PLACE YOUR ADS HERE For more updates about Personal Development, Financial and Investment Education. Join and Subscribe to my Newsletter. It's FREE! ABOUT THE BLOGGER

Hi, I'm Ralph Gregore Masalihit! An RFP Graduate (Registered Financial Planner Institute - Philippines). A Personal Finance Advocate. An I.T. by Profession. An Investor. Business Minded. An Introvert. A Photography Enthusiast. A Travel and Personal Finance Blogger (Lakbay Diwa and Kuripot Pinoy). Currently, I'm working my way toward time and financial freedom. Connect

|