Personal Development, Business, Finance, and Investing for Everyone

An investment in knowledge always pays the best interest.

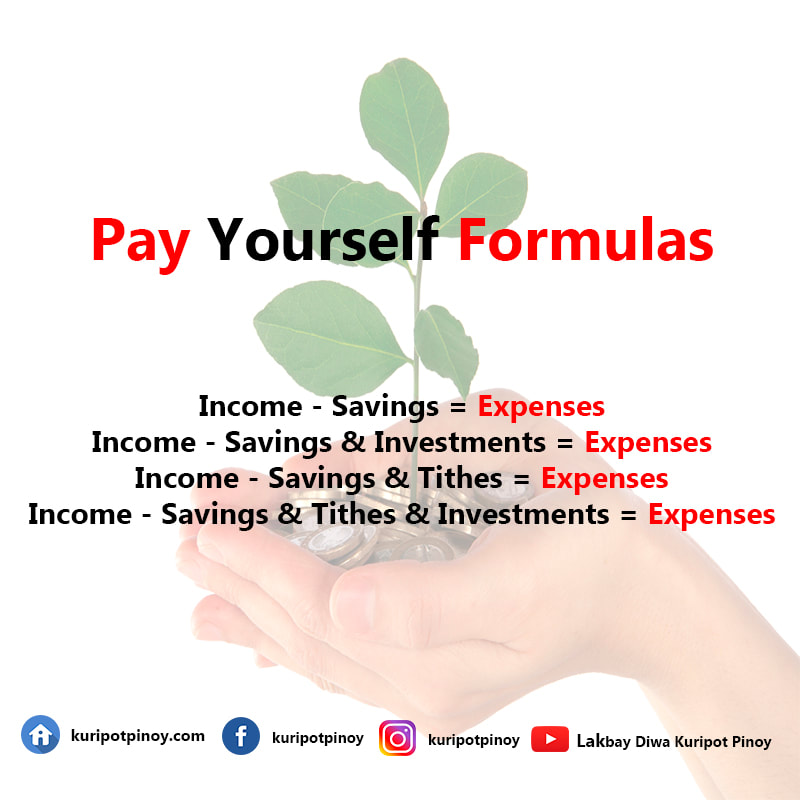

Financial literacy is an understanding of the many facets involved with personal finance such as spending, saving, and investing. For everyone, a grasp on the basic concepts is important as the knowledge will not only prove necessary all throughout life, it also has the power to help individuals towards economic prosperity. For those who know very little about basic finances, the question becomes where to start and how to apply what is learned to everyday life. To aid in that, the following are some important concepts that should help to establish a sound base from which you can continue to grow and refine your understanding. Saving For many of us, the idea of storing money away is not a new one. When it comes to financial literacy however, there are several important facts about saving that people may or may not be aware of. The first is the idea of building up savings within a bank. Typically done through a savings account, this allows individuals to build up their funds in a safe place. In addition to holding our money, savings accounts can accrue very small amounts of interest each month. In this case, interest is money that is gradually amassed without you having to lift a finger. Savings accounts differ from checking accounts which are typically tapped for daily transactions, automatic deposits, and withdrawals using the ATM. In terms of keeping up with your savings account, some banks require a minimum balance to be held within the account at all times. Savings accounts are advantageous because they can act as a separate place in which to store money that is more out of reach than a checking account. You can open up multiple savings accounts to allow for separate prioritization of financial goals, devoting one account to the likes of saving up for a move while another may be for a trip. Along with the simple act of creating a savings account, one of the most important things that you can do with your money is create an emergency fund. An emergency fund is an account that you should contribute to regularly that is meant to act as a safety net for you and your loved ones should something unexpected happen. This can include an untimely death, an unexpected injury or illness, or other significant expenses incurred, such as a car repair. The goal of the savings account is to grow it, as the larger it is, the more protection and flexibility it allows. It is important to understand that emergency funds should not be touched until the time in which a crisis arises as tapping it before then undermines what it represents. In saving within it, you should aim to have at least half your annual paycheck put away after some time of saving. If you can save even more, say the equivalent of one year’s pay, then you will have put yourself in a great position financially. Budgeting Part of having money to save up relates to budgeting, which is the skillful allocation of money for different purposes. The process of creating a budget involves determining where your money is being spent and how you can reorganize your spending, whether that means cutting back on things or cutting some things off entirely in order to come up with the funds you need. To get started with this, you should first take a week or so to track how you are currently doing your spending. Are the majority of your funds going to necessities or luxuries? Be sure to be specific, including information like what you’re spending on and the amount you’re purchasing. Once you have an idea of that information, you will want to go through your notes and see where you’re spending the most. Identify if those costs are necessary or not and determine how much you can cut back. Often times, doing things like switching from brand name to generic ones or implementing changes in your everyday life can be extremely advantageous. In addition, saving can be done in the home as cutting down on energy usage and finding ways to save electricity will guarantee you some form of savings that can be used elsewhere. More than anything, your budget will act as a financial guide. It may take some time before you have complete control over everything as you have it outlined, but the key is to stick to the plan and hold yourself accountable. As you get better with using your budget and find that you can do even more saving, you can adjust your budget to account for your increase in funds. As you put your money towards various activities, make sure you are regularly contributing to your emergency fund as that protection is crucial for your financial health. Credit Credit is essentially an agreement made between two parties in which one acquires goods or services from the other without paying for them initially with the understanding there will be reimbursement at later time. There are several ways through which credit can be used, and it often takes the form of a credit card, where by swiping and signing individuals are able to complete transactions before receiving monthly bills stating how much they owe. Often included in the terms of this is interest, which differs from the interest mentioned before with the savings account. This interest instead refers to an additional charge for the price of goods that increases the expense the longer the borrowed money goes unpaid. When it comes to credit, it is critical that individuals be responsible. A number of countries assign credit scores which are numerical values that indicate overall creditworthiness. The worse your score, the less likely you will be to qualify for the use of credit. In the event you do have a poor score, your interest rates will be higher than they would have had your score been better. Interest rates are amounts that are noted as percentages that are charged on top of the initial sum owed. Interests rates often come into play for large assets like vehicles and homes. For those looking to start building their credit or improve their credit score, demonstrating sound use of credit is important. This means using credit and paying back what is owed in a timely manner. Something to note about credit scores is that checking them can actually lower them for a time. This depends on the type of inquiry made to check it though. A hard inquiry occurs when institutions are trying to determine if they should issue you credit. This is common for things like a credit card, loan, or mortgage. One hard inquiry should not cause any major shifts in your credit score, but multiple ones in quick succession can. Soft inquiries on the other hand will not affect your credit score and can occur during slightly less serious financial endeavors, like when a possible employer conducts a background check. Debt Debt refers to a state of being in which money is owed to someone or something. Debt comes in many forms including credit card debt, student loan debt, and medical debt as well. In terms of financial literacy, though there are forms of good debt which refers to things that increase in value, it is best to minimize the amount that is taken on when possible. In life however, it is likely that debt will have to be taken on in one form or another. In such instances there are several methods for paying it off, especially if you are facing several debt-based expenses and need to prioritize one over the other. Before that however, it is important to note that if you are ever to make the full payments in order to eliminate debt instead of relying minimum payments, do so, as it will reduce the time and money that you must pay. Going above and beyond and paying more will also expedite the repayment process. When it comes to multiple sources of debt competing for your attention, there are two ways to go about paying them off. The first involves prioritizing the total, so in the event your student loans total Php 300,000 and you owe Php 50,000 on one credit card and Php 70,000 on another, you can make smaller contributions or even the minimum payment to the credit cards if necessary, while paying the full amount on the student loans. The other method involves paying based on interest rate. In this case you’ll want to prioritize the sources with the highest rate and pay the full amount on those while managing the others. If the rate on your student loans is 2% while credit card one is 5% and credit card two is 3%, prioritize fully paying off credit card one, then credit card two, and finally your student loans. Investing For those hoping to grow their money, investing is method of doing so which involves placing sums in different endeavors that carry various amounts of risk. In this context, risk refers to the likelihood that the returns on investments will vary from what is expected. Typically, the greater the risk, the greater the possible reward. When it comes to investing, there are several things to note and several ways to go about doing so. The term invest makes most people think of the stock market where stocks, or shares of ownership in a company, can be bought and sold. The value of stocks change on a daily basis based on many variables and there are different kinds of stocks, though the main two are preferred stock and common stock. They entail different rights and can include the ability to receive dividends, which are sums of money paid to shareholders on a regular basis. Individuals can also invest in mutual funds, which are collectives made up of the money from a number of investors that invest in stocks and bonds and are handled by financial professionals who are working to produce profits for investors. Along with stocks and mutual funds are bonds, which are low risk investments where money is given to a company or the government for a prespecified amount of time, during which interest payments will be made and at the conclusion of which, the maturity date, the initial investment is returned. Bonds are also known as fixed-income investments. While this is valuable information, it only scratches the surface of investment and all that it entails. It also reinforces the fact that when it comes to financial literacy, there is a lot to learn and it is a continued process of growth as individuals expand into the many arenas it encompasses. As result, it is important to continue to refine your knowledge and find new opportunities to learn.

0 Comments

Leave a Reply. |

PLACE YOUR ADS HERE YOUR PAYDAY REMINDER

FEATURED PARTNER

FEATURED PROMOTIONS

FEATURED MENTIONS

PLACE YOUR ADS HERE PLACE YOUR ADS HERE For more updates about Personal Development, Financial and Investment Education. Join and Subscribe to my Newsletter. It's FREE! ABOUT THE BLOGGER

Hi, I'm Ralph Gregore Masalihit! An RFP Graduate (Registered Financial Planner Institute - Philippines). A Personal Finance Advocate. An I.T. by Profession. An Investor. Business Minded. An Introvert. A Photography Enthusiast. A Travel and Personal Finance Blogger (Lakbay Diwa and Kuripot Pinoy). Currently, I'm working my way toward time and financial freedom. Connect

|